The A on the front door of Lake Pavilion beckoned like a flashing welcome sign. And we happily turned on to a block off of Main Street in Flushing to find parking. The idea of yummy Chinese dim sum made us smile and delighted us to learn that this Chinese restaurant earns an A from the New York City Health Department.

Delicate shrimp dumplings, shrimp wrapped in silky rice noodles, pork in thin tofu skin with a syrupy glaze, eggplant stuffed with shrimp, salt baked skinny fish, chunks of boneless chicken, thick pork puns, hacked up sweet spareribs, mounds of noodles and greens fill the carts the ladies wheel between tables. And we wanted a taste of it all.

We stopped visiting Lake Pavilion after a scathing health department report in the fall of 2014. Even though the restaurant cleaned up quickly and got the all-clear from the health department, we couldn’t bring ourselves to eat there right away.

But on this Sunday morning, we made a trip to a nearby Costco, in Rego Park, to load up on household cleaning stuff and paper goods, and decided to swing by the restaurant to check it out again.

Lake Pavilion fills the old Palace diner right off the Long Island Expressway and you can’t beat the convenient location. The bright, sun-filled restaurant looked spotless when we arrived. Our timing seemed pretty good. Only a handful of people waited around the reception desk. While the main room and all the little side rooms were full, the wait was only about five minutes.

Frequently, we share a table with others. But this time, we got a table for two jammed in between two big tables filled with families. And the food started coming almost as soon as we sat down.

The ladies wheeled their carts with the steaming bamboo containers filled with everything we love to eat and tried to explain dishes we hadn’t tasted before.

Dim Sum Dishes from Lake Pavilion in Flushing Queens. Photo by ConsumerMojo.com

My husband Nick puts fiery spicy red sauce and mustard on most of the food he eats for lunch. But I love the delicate taste of the naked, plump dumplings and it all tasted just right to me. Nick held off on dumping the sauce on the delicate tofu skin rolls stuffed with pork. “This dish doesn’t need anything,” he said.

Now we plan to visit Lake Pavilion for dinner when the seafood menu shines. We’ll tell you about that in the coming weeks.

Our mom loved good jewelry and my sister and I bought her pretty things for Mother’s Day and her birthday. Looking back, it’s amazing to me that we managed to buy gold jewelry without getting ripped off.

I’m the big sister and the shopper in the family and remember starting the tradition when I was in high school.

On one shopping trip in the 47th Street Diamond District in Manhattan, around the corner from my high school, I found a gold abstract bird pin. Its eye was a tiny ruby chip and I thought the pin was perfect. It turned out our mom did too.

But how did I know it was gold? I really didn’t. I thought I knew because I had watched my mother inspect stamps on the back of jewelry, looking for the 14K sign, for years. I did the same. How did I know it was a real ruby? I had no idea.

Basically, I shopped with faith, and that’s not such a good idea. Shakespeare knew what he was talking about when he wrote, “All that glitters is not gold.”

Long after my teenager jewelry buying, as a reporter I investigated jewelry sales and found some ugly practices. My team and I discovered some unscrupulous jewelers sold fake gold and phony gemstones.

That’s why I’m sharing a few basic facts. We put together a simple guide to help you buy jewelry for mom without getting ripped off.

SIMPLE GUY TO BUY JEWELRY

Courtesy Wikimedia

1. Decide how much you want to spend in advance so that you can avoid getting pushed into buying something that costs more than you had in mind. Sales people are often persuasive, maybe too persuasive.

2. Think about the type of jewelry that you’d like to buy. This will allow you to be in control and avoid feeling overwhelmed when you get to the jewelry counter.

3. Don’t buy anything on impulse. Take time to think about it and maybe even comparison shop.

4. Research the stores where you think you’ll shop. Check the store’s reputation online. Ask friends, or relatives for recommendations.

5. Study up to learn the terms that jewelers use. What’s 14K, 18K, 22,K- for example. Once you understand what the jeweler is talking about, you’ll get an idea about whether what you want to buy is worth the price.

6. Understand the refund and return policies before you buy. Can you get your money back, or must you exchange it for something else. Make sure you get a receipt and that the phone number is visible on the receipt. Sales receipts should have information about the jewelry including a gemological report from a laboratory.

The Jewelers Vigilance Committee offers this excellent information about jewelry:

Diamonds

The Four C’s are the criteria used to value a diamond. Ask about the carat weight, color, clarity and cut (cut refers to the quality of cut, not the shape).

Ask if the diamond(s) have been treated in any way (i.e. fracture-filled, laser drilled) and whether or not the treatment is permanent.

Colored Gemstones

Is the gemstone natural, lab created or an imitation?

Has this gemstone been treated? If so, how?

If treated, is the treatment permanent and has the treatment affected the gemstone’s value?

What is the country of origin of the gemstone?

Is special care required?

Pearls

Are the pearl(s) natural or cultured?

Has the pearl been dyed to enhance or change its color?

If the pearl is dyed, is the treatment permanent? Did this affect the value?

Is special care required?

Precious Metals

In addition to the specifics about precious metals, make sure that jewelry containing precious metal(s) is marked in compliance with the law.

The item’s karatage must be identified to you in some way (verbally, through signage, etc.).

If an item is stamped to indicate the quality of metal it contains, it must have a trademark in close proximity to the quality mark. (A trademark is a symbol stamped next to the quality mark and may be initials or a logo to identity the make of the item.)Platinum

Items containing 950 parts per thousand (95%) may be marked as platinum.

Items that are 85% or 95% platinum must be marked with the platinum content. Examples: 900Pt, 850Pt.

Items containing less than 85% platinum must detail the platinum group metal. Example: 750Pt200Irid. Total parts must equal 950 (95%). Note: Platinum group metals are: Platinum, Palladium, Rhodium, Iridium, Ruthenium and Osmium.Gold

10 karat gold is the minimum fineness of gold that may be sold in the U.S. Jewelry under 10kt fineness may not be sold as gold.

Jewelry is made of many different types of gold: solid gold, gold plate, gold filled, gold overlay, gold electroplate, gold flashed/washed or rolled gold plated.Silver

Silver/Sterling Silver means that 925 parts per thousand (or 92.5%) of the item is made of pure silver.

Silver plate describes a product made of base metal and layered (or plated) with silver.

Silver coins contain 900 parts per thousand (or 90%) pure silver.

You wonder why some people don’t get sent directly to jail. The Brooklyn man behind the Instant Response System, or IRS, medical alert service wins my nomination.

True, it’s a good thing that a federal judge ordered the Instant Response medical alert scam shut down. But shouldn’t the scammer pay a bigger price?

IRS mastermind Jason, or Yaakov, Abraham targeted adults over 70 who lived alone on fixed incomes. He wrote a script and hired telemarketers to sell them a medical alert pendant that would supposedly provide 24-hour service seven days a week.

Telemarketers asked a series of questions like:

Have you ever fallen down?

Do you have dizzy spells?

How long did you lie there before being found?

What would happen if you were not found?

The telemarketers played on peoples’ worst fears and told them the pendant would cost between $817 and $1,602.

Once people gave their names and addresses, IRS shipped the pendants and the harassment for payment began, even if people never ordered the pendants.

Telemarketers repeatedly threatened physical injury, financial ruin and even the possibility of jail time. They also sent threatening letters and phony police reports to people who refused to bend to the intimidation.

The threats got results. Abraham and IRS took in more than $3.4 million from consumers, according to the Federal Trade Commission (FTC). The agency sued IRS and asked a federal judge to permanently shut down the business.

Judge I. Leo Glasser in the Eastern District of New York agreed with the FTC and found that Abraham “…knowingly made misrepresentations to hundreds of consumers over a five-year period.” He also pointed out that in 2003 a federal judge in Washington, D.C., shut down an Abraham scam that marketed fake international driver’s permits and barred Abraham from engaging in telemarketing.

The judge ordered that the $3.4 million IRS took in should go back to the hundreds of consumers all across the country who forked out the money.

But we think Jason (Yaakov) Abraham deserves a stiffer penalty.

The latest news from the New York Federal Reserve Bank confirms suspicions about the burden of student loans, especially in New York City. The Regional Household Debt and Credit Snapshot found the average student loan debt was $34,300 during the last quarter of 2014.

The latest numbers on student loan debt support calls for reform by advocates like Senator Elizabeth Warren. The Massachusetts Democrat proposed a law to make it as easy to refinance a student loan as it is to refinance a mortgage.That would give students a real shot at lowering the interest rates on their loans when interest rates go down. Right now, they’re stuck with paying relatively high interest rates.

New York City students have more reason than most to root for a plan to refinance their college loans. The Fed study found that debt for students in the city is higher than for those throughout the state who carry an average balance of $31,000. And it’s higher than the national average of about $28,000.

College loan delinquencies plague New Yorkers. The most troubling statistic in the Fed’s analysis reveals that 14.7 percent of city student loan holders were seriously delinquent in the last half of the year. That means they hadn’t made a payment in 90 days or more.

Depressingly, researchers found student loan delinquencies surpass credit card and mortgage delinquencies.

President Obama issued an executive order in June of 2014 that should help some. About 5 million people nationwide will get an opportunity to tie their monthly payments to what they earn. This means your loan payment could be capped at 10 percent of your monthly income starting in December 2015. The order covers those who borrowed money between October 2007 and October 2011.

Figuring out when to enroll in Medicare may sound simple enough. But in fact, Medicare enrollment gets complicated. And if you don’t sign up for Medicare Part B when the formal schedule requires you to, it will cost you extra money every year of your life.

That’s why the Medicare Rights Center called for changes and improvements in the enrollment process. It issued a call for better notification for the 10,000 Baby Boomers who turn 65 every day, more support for employers, and a better appeals process if you make a mistake.

Many of us don’t know the rules and the consequences for failing to follow them.

For example, if you turn 65 and you or your spouse stopped working and have coverage under Cobra or another extended insurance plan, you still need to sign up for Medicare B right away. You have a seven-month window: three months before your birth month, your birth month, and three months after.

Even if you have insurance under your spouse’s plan and you are not working, you need to sign up for Part B during the open enrollment period.

Why? Medicare will penalize you, and charge you extra for Part B insurance for the rest of of your life. You also may end up without insurance until the next open enrollment period.

Because: You can only ignore the specific enrollment period if you are “actively employed” and have health insurance coverage from your employer. Medicare specifically rules out part-time employment and coverage from another insurance source.

Barry Galkin, an insurance consultant who specializes in Medicare-related issues says, “There have been cases that I’ve heard of where people who were 65 and still employed did not sign up for Part B. When they had medical issues, their insurers refused to pay anything at all because they were not signed up for Part B.”

The Medicare Rights Center suggests:

1. Start to think about Medicare six months before your 65th birthday.

2. Make an appointment to talk to someone in your local Social Security office, or an insurance broker or advisor.

3. Write down what people tell you so that you can review and make sure you understand the details.

4. Consider enrolling in Medicare Part B even if you are still working and are covered by your employer.

5. If you have an unusual situation, don’t assume the general rules apply to you. Ask a lot of questions.

The offers keep coming and every time one hits my desk, I wonder if these people who want to lend me money, or help me get long-term care, or sell me an annuity have my best interests at heart.

When I opened the latest piece of mail, I asked the obvious question: “Why did the bank offer me $25,000?”

Maybe it’s because I’m older and maybe it’s because my financial history looks more than okay. But hey, taking any or all of the offers might just ruin my future financial life.

I’m troubled particularly because many of the offers come from, or use the names of, reputable organizations. In three instances, the offers came through a couple of unions that list me as a member.

So if I were a less skeptical person, I might think that the union actually endorsed the idea of my borrowing $25,000 to consolidate my bills. But I look at these offers and toss them in the trash, and I’m glad that I don’t need to rush to borrow.

The long-term care letters also make you pause, because you’re asked to bet that if you pay money now, you’ll need the insurance payout that builds up in your later years.

Long term care may sound like a good idea because Medicare doesn’t pay for what it considers “custodial services.” In other words non-medical help that you might need.

With long-term care insurance you pay a monthly fee and then when you need the insurance it’s supposed to pay for:

Caregiver Services

Assisted Living Facilities

Hospice Care

Nursing Homes

Adult Day Services

Skilled Nursing At Home

Physical And Speech Therapy At Home

Help With Bathing and Dressing At Home

But what if it ends up that you don’t need any of those things? Instead, you need money to pay your taxes, or your rent?

And it also turns out that some policies come with rules and regulations that make it tough to collect the money. A New York Times story detailed the nightmare one family experienced trying to collect for assisted living.

So maybe when we think it through, we want to save our money, or invest to pay for future problems in another way.

I’m not saying a consolidation loan is wrong. Or that long-term care insurance doesn’t pay off. Maybe some of the other solicitations are great too.

But I am saying it is wrong for organizations we trust to let companies send us these alluring come-ons without including caveats or warnings that the plans and schemes may not work for everyone and come with significant risk in some cases.

The Consumer Financial Protection Bureau says that older adults are “prime targets for financial exploitation,” and calls the financial abuse of seniors an “under the radar epidemic.”

So maybe it’s time to get proactive before it’s too late. Those of us, particularly Baby Boomers, who still have our wits about us, might want kick into activism mode. Why not let the unions, colleges and groups that we belong to know that we don’t like it when they lend their names to these mailings that don’t include the full story and could lead to our exploitation.

I’m always surprised at how scammers play the same games over and over again. They develop a new twist here and there and when law enforcement cracks down on one of them a new set of crooks pops up with a variation on the old game.

You get a good idea of scammers’ favorite games when you take a look the Federal Trade Commission’s (FTC) list of top ten scams for 2014.

Identity theft leads the list. That should come as no surprise to anyone in light of the hacking and data theft that occurred at retailers and insurance companies within the past year.

Someone just needs your Social Security number to steal your identity, open a bank account, get a credit card and file an income tax claim in your name. And while many of us may hug our Social Security numbers closely, we are all easy victims when hackers get into a big system that contains all of our information.

Imposter Scams appear in third place on the top ten list and they include the IRS scam that ConsumerMojo warns about regularly.

Jessica Rich, director of the FTC’s Bureau of Consumer Protection, said, “Consumers should…keep a close eye out for imposter scams. Whether it’s pretending to be the IRS during tax season, or making false promises of a lottery win, scammers are increasingly sophisticated in their efforts to deceive consumers.”

If you owe money and fell behind, it’s important to know your rights when the debt collector calls.

Lawyer Susan Shin with the New Economy Project formerly Neighborhood Economic Development Advocacy Project ( NEDAP), says that federal law gives you the right to stop debt collectors from contacting you. If you write to a debt collector to say you don’t want them to contact you, they must stop. But if you owe money, this doesn’t mean the debt goes away.

There is still a possibility you could be sued for the debt. You also have the right to dispute the debt, in writing, and demand that the debt collector verify it.

Verification means that debt collector gives you enough information so that you can determine if you actually owe the money.

If you make this request for verification within 30 days of receiving the initial written communication from the debt collector, the collector must verify the debt or else stop all collection efforts against you for the disputed debt, according to federal law. Very simply, if you don’t recognize the debt or if you want to dispute the debt, you can send a letter to the debt collector and say so.

Debt collectors are not allowed to call you before 8 in the morning or after 9 at night. They can’t call you at work if you tell them not to.

They also can’t make false threats, such as saying that you’ll be arrested if you don’t pay. They can’t make false claims to you while they are trying to collect, or pretend to be lawyers or law enforcement officials.

If you think you are being treated unfairly or if you think a debt collector is violating the law, contact your state attorney general and also file a complaint with the Consumer Financial Protection Bureau and the Federal Trade Commission.

If you trust your investment advisor, great. But you may want to take a second look and ask some hard questions about the way the investment advisor you use does business.

President Obama plans to introduce new rules in the next few weeks that crack down on conflicts of interest by investment advisors.

The President’s Council of Economic Advisors found a sharp decline in the number of Americans who get retirement income from pensions. Instead, a growing number of people depend on investments like 401(k’s) and IRA’s.

More than 40 million American families trust, collectively, more than $7 trillion to IRA’s.

Economic researchers found investment advisors often have hidden conflicts of interest. And that doesn’t turn out well for you.

Conflicted advice leads to lower investment returns. Savers receiving conflicted advice earn returns roughly 1 percentage point lower each year.

Many investment advisors get paid for selling the so-called “products” they sell you.The Council of Economic Advisors estimates “the aggregate annual cost of conflicted advice is about $17 billion each year.

The conflicts lead to big losses.The Council of Economic Advisors says, “A retiree who receives conflicted advice when rolling over a 401(k) balance to an IRA at retirement will lose an estimated 12 percent of the value of his or her savings if drawn down over 30 years.”

And there’s more. “The average IRA rollover for individuals 55 to 64 in 2012 was more than $100,000; losing 12 percent from conflicted advice has the same effect on feasible future withdrawals as if $12,000 was lost in the transfer.”

Here’s what you need to do.

1. Ask questions of your advisor.

2. Make sure his or her conflicts of interest don’t cost you money.

3. Get second opinions.

The Obama administration fix won’t come quickly. It must go through a rule making process and the Department of Labor will be in charge. It will ask for public input. You put in your two cents.

And then, the administration will issue a rule that will attempt to reign in the wild west style of some of these financial advisors.

Francisco Curiel hoped to apply for an immigration relief program that would grant him a Social Security card and a work permit. When a federal judge halted expansion of the Obama administration program, he was shocked. “Is this for real?” he asked himself and everyone else who would listen.

“This is not a game. This is my future and I don’t think it’s fair,” the 22-year-old immigrant from Mexico told ConsumerMojo.

On Friday, the White House said it will seek an appeal and asked for a temporary stay of Judge Andrew Hanen’s ruling.

You may question whether the judge’s decision is political or raises a true constitutional question about President Obama’s right to use an executive order to legitimize the U.S. life of nearly five million immigrants.

But for immigrants like Curiel, the ruling blocks the chance “to get that nine-digit card (Social Security card) and come out of the shadows.”

Curiel couldn’t apply for the previous DACA program because he came to the U.S. two months after the cut-off date. Under the new plans both he and his mom qualify.

But let us fill you on the back story. The ruling came in response to a lawsuit filed by Texas and 25 other states in Federal District Court in Brownsville, Texas.

The states asked Judge Hanen, an outspoken critic of President Obama, to halt his plan to expand his Deferred Action for Childhood Arrivals (DACA) program and implement another to give legal rights to parents of those with legal status and others who qualify.

Expansion of the DACA program was set to begin soon, and the administration planned the next phase for parents and others to begin in May.

Immigrant groups in Texas, New York and across the country issued calls to keep the faith and promised to continue to fight for immigration reform.

Antonio Alarcon, of Make the Road New York said, “As an organizer and DREAMER we are going to continue fighting for DACA and DAPA (the adult program) implementations. We knew the judge was anti-immigrant and we were expecting that.”

A spokesperson for the New York Immigration Coalition told ConsumerMojo that he hopes people will continue to get ready to apply for these programs. “There is no harm in immigrants preparing their documents in order to prepare.” This would make it easier for people to apply once the executive order is in force again.

Francisco Curiel gets the last word. “I don’t think it’s defeat. It’s a challenge we must continue to fight,” he told us.

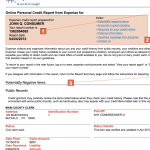

If you’re confused about the difference between your credit score and your credit report you’re not alone.

The Consumer Financial Protection Bureau (CFPB) says more than 50 million people now can access their credit reports and credit scores but many of us wonder what we’re looking at.

Here’s how it shakes out:

Credit Report:

Your credit report is a record of your financial history. It lists all of your credit cards, your payment history and any money that you owe.

Three major credit bureaus, private companies, keep track of all of this information and share it with people who pay for it. You can get a free look at your credit report three times a year at annualcreditreport.com.

Experian, TransUnion and Equinox run these sites and the law requires them to provide a free credit report to you each year. So again, don’t pay anyone for a credit report; you can get one for free.

Credit Score:

Your credit score is more complicated. It’s a statistical analysis of your outstanding debt, credit history and payment history. Most banks and other financial institutions look at the credit score compiled by FICO or the Fair Isaac Corporation. It’s another private company that keeps tabs on you. FICo gives you access to your Credit Score for a fee.

Last year, the CFPB asked credit card companies and financial institutions to make your credit score available to you for free. More than a dozen companies complied with the request and others seem headed in that direction.

CFPB Director Richard Corday said, “Access to these scores provides an opportunity to engage consumers around their credit reports. Once consumers see their credit scores, they can be motivated to learn more about their credit history, check their full credit report, and take action to improve their financial lives.”

IMPACT

Because your credit report is the basis of your credit score, it’s important to check your credit report for errors because what’s on your credit report can have a huge impact on your life. It goes way beyond whether or not you can apply for a credit card or get a loan.

WHO CHECKS CREDIT REPORTS

Landlords, employers, utility companies, you name it use the credit report to examine your payment history. And unfortunately there are often mistakes and errors on the report.

So make sure that everything on the report is accurate. If details are wrong, if debts are listed incorrectly, if it shows that you owe money when you don’t, dispute the errors.

When gas prices hovered around the $2.00 mark, even dipping below that in 24 states, a lot of us had reason to applaud. But the applause fades quickly and don’t we want to know the future of gas prices?

A new survey from the Consumer Federation of America (CFA) found most think gas prices will keep going up and 86 percent of those polled say it’s a reason to buy a more fuel-efficient vehicle.

CFA says consumers expect the national gasoline price average to rise by almost 50 percent in the next two years – from about $2.14 to $3.20 – and by over 80 percent in the next five years – to $3.90.

But AAA puts a little perspective on things and points out that “ample gasoline supplies and lower crude oil costs than in recent years should prevent prices from rising as high as in recent memory.”

AAA projects that we’ll continue to pay less than $3.00 a gallon for the rest of 2015.

Gas Price Envy

We may share a little gas price envy. Drivers in Utah, Idaho and Montana paid less than $2.00 a gallon as we wrote this post. The volatility of the oil market will change all of that, we expect.

And that brings us back to CFA and its suggestions for dealing with see-sawing gas prices. The advocacy group cautions us not to rush out and buy gas-guzzling vehicles just because there’s in a dip in prices.

Dr. Mark Cooper, CFA’s Director of Research said, “Buying an inefficient vehicle during periods of low gas prices condemns the consumer to wider swings in monthly costs, much higher monthly peaks, and a whopping overall increase in lifetime gas costs.”

You can improve your credit every day. Your credit life is a living, breathing thing and it changes as you pay your bills. If someone makes a mistake, or lies, and you find an incorrect negative item on your credit report, you can do something about it.

You can do something about it.

You can improve your credit report.

You can improve your credit score.

They both change all of the time.

LIES ABOUT FIXING YOUR CREDIT

You can fix your credit quickly.

You can pay someone to fix your credit

You can pay a company to fix your credit.

If you pay a debt settlement company you don’t have to pay your bills.

THE TRUTH ABOUT FIXING YOUR CREDIT

It takes time.

You need to pay your bills or negotiate to lower your bills so that you can make payments.

WHERE DO YOU START?You need to take a cold hard look at your credit report. You can get a freecopy of your credit report three times a year by going to AnnualCreditReport.com. Do not pay anyone to pull your credit report. You can do this by yourself.A federal law says that three credit reporting bureaus — Experian, TransUnion and Equifax — must make your credit report available to you. They teamed up to create AnnualCreditReport.com. Avoid other websites that promise to get your credit report.Or you can write and request a copy:

Annual Credit Report Request ServiceP.O. Box 105281Atlanta, GA 30348-5281

WHY SHOULD YOU CHECK YOUR CREDIT REPORT?It’s important to thoroughly review your credit report because prospective employers look at it, lenders look at it and many landlords use credit reports before they decide to rent to you. You also want to examine the report to:

See where you stand.

Make sure no one has opened accounts in your name.

Make sure the information on your credit report is accurate.

WHAT’S ON YOUR CREDIT REPORT?

Your credit report is a history of your financial life. It has your bill paying history. It lists and shows:

The credit cards you have, and your payment rate.

The loans you have, or had, and your loan payment history.

Your mortgage and your mortgage payments.

Student loans, you have or had, and the way you repay them.

Judgments or liens against you.

Alimony or child support payments and how you pay.

Money you may owe a doctor or healthcare provider.

Money you may owe a hospital.

Your outstanding parking ticket fines.

Whether you’ve been sued.

Whether you’ve been arrested.

The list will include all of your debts and financial activity and anything to do with your money. It is unlikely to include local retailers, gasoline credit card companies and landlords with just one or two properties.Inaccurate InformationCredit bureaus make mistakes. If there is a mistake, you must dispute it. You do this by sending letters with proof — your cancelled checks, credit card receipts or other proof that you have paid a bill.Experian-1-888-397-3742www.experian.comTransUnion-1-800-916-8800www.transunion.comEquifax-1-800-685-1111www.equifax.comThe Federal Trade Commission created a sample letter.

Or, you can use our version:

SAMPLE LETTER TO CREDIT BUREAU

Date

Your Name

Your Address, City, State, Zipe Code

Complaint DepartmentName of Company

Address

City, State, Zip Code

Dear Sir or Madam:

I am disputing the following information in my file. I have circled the items I dispute on the attached copy of the form that I received.This item (s) (List the item or items you’re disputing and the name of the source such as creditors or tax court and identify the type of account- credit card or judgment, etc.) is inaccurate or incomplete. (Describe what is inaccurate or incomplete and why). I am requesting that the item be removed to correct the information.Enclosed are copies of my documentation that support my position. (Describe what you enclose: receipts, payment stubs, court records, etc.)Please reinvestigate this matter (or these matters), and correct or delete the information as soon as possible.Sincerely,Your NameEnclosures: List all the documents that you are enclosing.Do not send originals. Send copies and keep a copy of your letter.Send the same letter to the creditor with the same documentation.

Send both by certified mail and keep your receipt.

CREDIT REPORTING COMPANIES MUST INVESTIGATE

Credit reporting companies must investigate within 30 days of receiving your letter. They also must send your dispute and your information to the company or organization involved.

That company is required to investigate and report back to the credit bureau.

If they find that you are right, the information must be corrected on your credit reports by all three reporting companies.

The credit reporting companies must give you the results in writing and a free copy of your updated credit report.

This doesn’t count as one of the three free annual credit reports.If there was an error, you can ask the credit reporting company to send a letter to companies or individuals who received a copy of your credit reporting within the previous six months.

If a company refuses to correct what you claim is an error, you can request that credit reporting bureau keep a copy of your statement in your file.

Theoretically, this should work. But many people have a great deal of trouble getting inaccurate negative information removed.

It is actively investigating the way credit bureaus keep their files and handle complaints.

HOW LONG DOES IT TAKE TO IMPROVE YOUR CREDIT?

Your credit gets better as you pay your bills. But if it is really bad, it will take seven years of regular on-time payments to clean everything up.If you had a bankruptcy, it will take ten years to clear your record.

YOUR CREDIT SCORE

What’s on your credit report is reflected in your credit score. Most banks and lenders use the FICO Score created by a private company called Fair Isaac Corporation. It developed a formula, or formulas for calculating your credit worthiness based upon the following.35 percent based on your payment history.30 percent based on the amount you owe.15 percent length of credit history.10 percent new cards.10 percent types of credit.

FICO TIPS:

Apply for and open credit accounts if you really need them.

Don’t open accounts just to have a new card.

Closing a credit card won’t make the debt go away.

In fact, if you close a credit card it’s likely to factor as a negative in your score. If you clear your bill and don’t ever use it, that may be a problem too. So it’s probably a good idea to pay one bill with it, and keep it in a drawer the rest of the time.

Also when you use your credit card, make sure that you don’t exceed 50 percent of the limit. If you go beyond 50 percent, bankers advise that you split the debt between two credit cards. That it is likely to improve your credit score.

HOW TO HANDLE OUTSTANDING DEBT

If you want to pay your bills but can’t make the monthly payments, NEGOTIATE.

A company will write off your debt after 180 days, but it is still held against you and you will still have to pay.The company would rather have your money than write off the debt. It’s better for you and them, if you negotiate.

Here’s what to do:

Call the customer service number on the back of the bill.Be very polite. Say that you would like to set up a payment plan.See if you can negotiate a sum that you can actually afford.If the person on the other end of the phone won’t help you, ask to talk to supervisor.

Don’t lose your temper.

Explain what you want. You are likely to get it.

If you don’t, do a Google search. Find the name of the company president and the address and write a letter explaining what you want to do.

Happy Year of the Sheep 2015, or is the goat or the ram? Chinese astrology sites lump all three together. But let the sheep take the astrological leading role and describe the year it represents as a more peaceful time and period of positive change.

The Chinese use twelve animals for predictions and sheep takes eighth place in the Chinese zodiac system that dates to the Han Dynasty from 206 BC to 220 BC. And whether astrologers refer to the animal as a goat or a ram, some call it a “lucky animal” because it doesn’t have to do heavy farm work like the Ox.

To make things even more confusing, the Chinese also describe it as the “Year of the Green or Wooden Sheep.” Nevertheless, they suggest the animal that falls in the eighth spot is lucky and consequently luck will brush anyone born in the eighth month with good fortune.

The sheep falls into Yin or peaceful category as opposed to the more aggressive Yang.

The astrologers describe people born in the Year of the Sheep as gentle, elegant, artistic, caring. But there’s always the caution that sheep-born should make sure to assert themselves when necessary.

Travel Guide China lists a varied group of celebrities born in the year of the sheep and they include: Thomas Edison, Orville Wright, Mark Twain, Barbara Walters, Julia Roberts, Matt Le Blanc, Nicole Kidman, Claire Danes, Bruce Willis and Benicio Del Toro.

So creative, inventive clever people represent the best of the “Year of the Sheep.”

The bottom line for most fortune tellers suggests that “goodness brings…fortune,” and that’s a lovely way to look at the year ahead for all of us.

And for all of our young Chinese friends, we hope you find fortune in your red envelopes.

Valentine’s Day jewelry ads seductively work their magic and get us to think about buying, receiving and wearing something gold or glittery. It’s all good, if you know what you’re doing when you go shopping.

When I worked on TV, the run-up to Valentine’s Day always led us to investigate claims from stores, big and small, and predictably we uncovered some people who didn’t sell what they advertised. In the stores with questionable practices, we frequently found that some gold jewelry didn’t weigh as much as claimed. And in some, we found so-called gold jewelry that wasn’t gold at all.

So it’s a good idea to take care when you shop. And that’s why we put together this tip sheet on how to avoid Valentine’s Day jewelry scams.

Here are 6 Valentine’s Day Jewelry Tips

1. Decide how much you want to spend in advance so that you can avoid getting pushed into buying something that costs more than you had in mind. Sales people are often persuasive, maybe too persuasive.

2. Think in advance about the type of jewelry that you’d like to buy. This will allow you to be in control and avoid feeling overwhelmed when you get to the jewelry counter.

3. Don’t buy anything on impulse. Take time to think about it and maybe even comparison shop.

4. Research the stores where you think you’ll shop. Check the store’s reputation online. Ask friends or relatives for recommendations.

5. Study up to learn the terms that jewelers use. What’s 14K, 18K, 22K, for example. Once you understand what the jeweler is talking about, you’ll get an idea whether what you want to buy is worth the price.

6. Understand the refund and return policies before you buy. Can you get your money back, or must you exchange it for something else? Make sure you get a receipt and that the phone number is visible on the receipt. Sales receipts should have information about the jewelry including a gemological report from a laboratory.

The Jewelers Vigilance Committee offers this excellent information about jewelry:

Diamonds

The Four C’s are the criteria used to value a diamond. Ask about the carat weight, color, clarity and cut (cut refers to the quality of cut, not the shape).

Ask if the diamond(s) have been treated in any way (i.e. fracture-filled, laser drilled) and whether or not the treatment is permanent.

Colored Gemstones

Is the gemstone natural, lab-created or an imitation?

Has this gemstone been treated? If so, how?

If treated, is the treatment permanent and has the treatment affected the gemstone’s value?

What is the country of origin of the gemstone?

Is special care required?

Pearls

Are the pearl(s) natural or cultured?

Has the pearl been dyed to enhance or change its color?

If the pearl is dyed, is the treatment permanent? Did this affect the value?

Is special care required?

Precious Metals

In addition to the specifics about precious metals, make sure that jewelry containing precious metal(s) is marked in compliance with the law.

The item’s karatage must be identified to you in some way (verbally, through signage, etc.).

If an item is stamped to indicate the quality of metal it contains, it must have a trademark in close proximity to the quality mark. (A trademark is a symbol stamped next to the quality mark and may be initials or a logo to identity the make of the item.)

Platinum

Items containing 950 parts per thousand (95%) may be marked as platinum.

Items that are between 85% and 94% platinum must be marked with the platinum content. Examples: 900Pt, 850Pt.

Items containing less than 85% platinum must detail the platinum group metal. Example: 750Pt200Irid. Total parts must equal 950 (95%). Note: Platinum group metals are: Platinum, Palladium, Rhodium, Iridium, Ruthenium and Osmium.

Gold

10 karat gold is the minimum fineness of gold that may be sold as gold in the U.S. Jewelry under 10kt fineness may not be sold as gold.

Jewelry is made of many different types of gold: solid gold, gold plate, gold filled, gold overlay, gold electroplate, gold flashed/washed or rolled gold plated.

Silver

Silver/Sterling Silver means that 925 parts per thousand (or 92.5%) of the item is made of pure silver.

Silver plate describes a product made of base metal and layered (or plated) with silver.

Silver coins contain 900 parts per thousand (or 90%) pure silver.

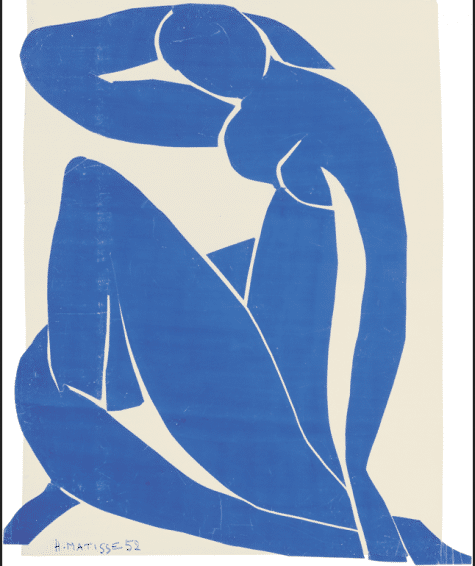

The work was done long ago, but it feels joyous, current and relevant. The Henri Matisse show, The Cut-Outs, at the Museum of Modern Art (MoMA) shows you the work of a master in the later years of his life.

The brilliant colors and playful shapes seem fresh and innovative and the exhibit presents Matisse as a life-force who continued to experiment and tease out ideas until the end. This celebration of a great artist offers inspiration about creativity and productivity. Matisse did most of the work when he was 77 to 84 years old. A short film in the exhibit shows Matisse in a hotel room in southern France, wearing pajamas and working from his wheelchair. Cancer surgery had made it difficult for him to move around. He uses a big scissors to cut and shape his figures and abstractions from colored sheets. You see him direct his young assistants to tack the work to the walls in his room and you get a feel for what it might have been like to be there. Matisse worked way beyond his limitations and pushed himself to do more. The show points out that he first used the cutout technique in the thirties to plan paintings. But the last incarnation of the cut-outs brought them to life in a new way. Palmetto Henri Matisse The brilliance of the later work attracted publishers and collectors and brought him a great deal of attention. Matisse created the well-known series of blue figures for the book called “Jazz” during this time. Yet after it publication, museum curators say he hated it because the prints didn’t show how the cut-outs had been arranged and rearranged to make them into art. But the show also displays work that Matisse loved and gave him great pleasure. The show itself seems put together by people who genuinely love the work and they share insightful anecdotes. For example, curators explain that Matisse wanted to see divers in a swimming pool and asked his assistant to take him to a public pool. But when they got there, he complained about the heat and the sun beating down on him. He announced that he would make his own swimming pool. So he and the assistant went home and Matisse went to work. He created a mural filled with whimsy for his dining room. MoMA owns the mural and restored it because it was deteriorating and the show was really put together to showcase this work. Now you can stand in a space the size of Matisse’s dining room and look up to share Matisse’s pleasure and see blue cutout figures, swimmers, who seem to glide through an imaginary pool. The show displays about 100 cut-outs and also includes the cut-outs used as models for stained glass windows and work commissioned for the patio of a Los Angeles couple. Every piece in the Matisse show delights and wandering through the galleries puts a smile on your face. But you can also take away five inspirations from the Matisse Cut-Outs.

5 INSPIRATIONS FROM THE MATISSE CUT-OUTS

1. TRY NEW THINGS

Matisse began creating the cut-outs when he was in his late seventies.

2. DO MORE THAN YOU THINK YOU CAN

Matisse continued to experiment and bring his ideas to life. The “Swimming Pool” is a great example.

3. SURROUND YOURSELF WITH COLOR

Matisse used brilliant blue, green, red, yellow and pink. He saw the world in his own form of Technicolor. A note in the show features a quote from Matisse apologizing to a catalog printer, “..for not having composed the catalogue cover in just three colors. It was not possible for me and I hope that its appeal for the public will allow you to sell enough copies to cover the cost of the printing.”

4. LET OTHERS HELP YOU, ESPECIALLY YOUNG AND VIBRANT PEOPLE

Matisse used young assistants to help him get around, organize things in his studio and pin-up the work on the walls. The notes in the show describe him as demanding.

5. PLEASE YOURSELF

When Matisse wasn’t satisfied with the work, he kept at it until it was right. You might also like this video about an artist working in France today: Living! Pierre Clerk

Delicate shrimp dumplings, shrimp wrapped in silky rice noodles, pork in thin tofu skin with a syrupy glaze, eggplant stuffed with shrimp, salt baked skinny fish, chunks of boneless chicken, thick pork puns, hacked up sweet spareribs, mounds of noodles and greens fill the carts the ladies wheel between tables. And we wanted a taste of it all.

Delicate shrimp dumplings, shrimp wrapped in silky rice noodles, pork in thin tofu skin with a syrupy glaze, eggplant stuffed with shrimp, salt baked skinny fish, chunks of boneless chicken, thick pork puns, hacked up sweet spareribs, mounds of noodles and greens fill the carts the ladies wheel between tables. And we wanted a taste of it all.

Items that are 85% or 95% platinum must be marked with the platinum content. Examples: 900Pt, 850Pt.

Items that are 85% or 95% platinum must be marked with the platinum content. Examples: 900Pt, 850Pt.

WHAT’S ON YOUR CREDIT REPORT?

WHAT’S ON YOUR CREDIT REPORT? 35 percent based on your payment history.

35 percent based on your payment history.

Has this gemstone been treated? If so, how?

Has this gemstone been treated? If so, how?

A short film in the exhibit shows Matisse in a hotel room in southern France, wearing pajamas and working from his wheelchair. Cancer surgery had made it difficult for him to move around. He uses a big scissors to cut and shape his figures and abstractions from colored sheets. You see him direct his young assistants to tack the work to the walls in his room and you get a feel for what it might have been like to be there. Matisse worked way beyond his limitations and pushed himself to do more. The show points out that he first used the cutout technique in the thirties to plan paintings. But the last incarnation of the cut-outs brought them to life in a new way.

A short film in the exhibit shows Matisse in a hotel room in southern France, wearing pajamas and working from his wheelchair. Cancer surgery had made it difficult for him to move around. He uses a big scissors to cut and shape his figures and abstractions from colored sheets. You see him direct his young assistants to tack the work to the walls in his room and you get a feel for what it might have been like to be there. Matisse worked way beyond his limitations and pushed himself to do more. The show points out that he first used the cutout technique in the thirties to plan paintings. But the last incarnation of the cut-outs brought them to life in a new way.

The show displays about 100 cut-outs and also includes the cut-outs used as models for stained glass windows and work commissioned for the patio of a Los Angeles couple. Every piece in the Matisse show delights and wandering through the galleries puts a smile on your face. But you can also take away five inspirations from the Matisse Cut-Outs.

The show displays about 100 cut-outs and also includes the cut-outs used as models for stained glass windows and work commissioned for the patio of a Los Angeles couple. Every piece in the Matisse show delights and wandering through the galleries puts a smile on your face. But you can also take away five inspirations from the Matisse Cut-Outs.