You can improve your credit every day. Your credit life is a living, breathing thing and it changes as you pay your bills. If someone makes a mistake, or lies, and you find an incorrect negative item on your credit report, you can do something about it.

- You can do something about it.

- You can improve your credit report.

- You can improve your credit score.

They both change all of the time.

LIES ABOUT FIXING YOUR CREDIT

- You can fix your credit quickly.

- You can pay someone to fix your credit

- You can pay a company to fix your credit.

- If you pay a debt settlement company you don’t have to pay your bills.

THE TRUTH ABOUT FIXING YOUR CREDIT

- It takes time.

- You need to pay your bills or negotiate to lower your bills so that you can make payments.

WHERE DO YOU START? You need to take a cold hard look at your credit report. You can get a free copy of your credit report three times a year by going to AnnualCreditReport.com. Do not pay anyone to pull your credit report. You can do this by yourself. A federal law says that three credit reporting bureaus — Experian, TransUnion and Equifax — must make your credit report available to you. They teamed up to create AnnualCreditReport.com. Avoid other websites that promise to get your credit report. Or you can write and request a copy:

WHERE DO YOU START? You need to take a cold hard look at your credit report. You can get a free copy of your credit report three times a year by going to AnnualCreditReport.com. Do not pay anyone to pull your credit report. You can do this by yourself. A federal law says that three credit reporting bureaus — Experian, TransUnion and Equifax — must make your credit report available to you. They teamed up to create AnnualCreditReport.com. Avoid other websites that promise to get your credit report. Or you can write and request a copy:

WHY SHOULD YOU CHECK YOUR CREDIT REPORT? It’s important to thoroughly review your credit report because prospective employers look at it, lenders look at it and many landlords use credit reports before they decide to rent to you. You also want to examine the report to:

- See where you stand.

- Make sure no one has opened accounts in your name.

- Make sure the information on your credit report is accurate.

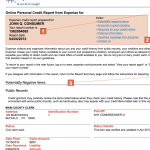

WHAT’S ON YOUR CREDIT REPORT?

WHAT’S ON YOUR CREDIT REPORT?

- Your credit report is a history of your financial life. It has your bill paying history. It lists and shows:

- The credit cards you have, and your payment rate.

- The loans you have, or had, and your loan payment history.

- Your mortgage and your mortgage payments.

- Student loans, you have or had, and the way you repay them.

- Judgments or liens against you.

- Alimony or child support payments and how you pay.

- Money you may owe a doctor or healthcare provider.

- Money you may owe a hospital.

- Your outstanding parking ticket fines.

- Whether you’ve been sued.

- Whether you’ve been arrested.

The list will include all of your debts and financial activity and anything to do with your money. It is unlikely to include local retailers, gasoline credit card companies and landlords with just one or two properties. Inaccurate Information Credit bureaus make mistakes. If there is a mistake, you must dispute it. You do this by sending letters with proof — your cancelled checks, credit card receipts or other proof that you have paid a bill. Experian-1-888-397-3742 www.experian.com TransUnion-1-800-916-8800 www.transunion.com Equifax-1-800-685-1111 www.equifax.com The Federal Trade Commission created a sample letter.

Or, you can use our version:

SAMPLE LETTER TO CREDIT BUREAU

Date

Your Name

Your Address, City, State, Zipe Code

Complaint Department Name of Company

Address

City, State, Zip Code

Dear Sir or Madam:

I am disputing the following information in my file. I have circled the items I dispute on the attached copy of the form that I received. This item (s) (List the item or items you’re disputing and the name of the source such as creditors or tax court and identify the type of account- credit card or judgment, etc.) is inaccurate or incomplete. (Describe what is inaccurate or incomplete and why). I am requesting that the item be removed to correct the information. Enclosed are copies of my documentation that support my position. (Describe what you enclose: receipts, payment stubs, court records, etc.) Please reinvestigate this matter (or these matters), and correct or delete the information as soon as possible. Sincerely, Your Name Enclosures: List all the documents that you are enclosing. Do not send originals. Send copies and keep a copy of your letter. Send the same letter to the creditor with the same documentation.

Send both by certified mail and keep your receipt.

CREDIT REPORTING COMPANIES MUST INVESTIGATE

Credit reporting companies must investigate within 30 days of receiving your letter. They also must send your dispute and your information to the company or organization involved.

That company is required to investigate and report back to the credit bureau.

If they find that you are right, the information must be corrected on your credit reports by all three reporting companies.

The credit reporting companies must give you the results in writing and a free copy of your updated credit report.

This doesn’t count as one of the three free annual credit reports. If there was an error, you can ask the credit reporting company to send a letter to companies or individuals who received a copy of your credit reporting within the previous six months.

If a company refuses to correct what you claim is an error, you can request that credit reporting bureau keep a copy of your statement in your file.

Theoretically, this should work. But many people have a great deal of trouble getting inaccurate negative information removed.

If you have a problem, file a complaint with the Consumer Financial Protection Bureau (CFPB).

It is actively investigating the way credit bureaus keep their files and handle complaints.

HOW LONG DOES IT TAKE TO IMPROVE YOUR CREDIT?

Your credit gets better as you pay your bills. But if it is really bad, it will take seven years of regular on-time payments to clean everything up. If you had a bankruptcy, it will take ten years to clear your record.

YOUR CREDIT SCORE

What’s on your credit report is reflected in your credit score. Most banks and lenders use the FICO Score created by a private company called Fair Isaac Corporation. It developed a formula, or formulas for calculating your credit worthiness based upon the following.  35 percent based on your payment history. 30 percent based on the amount you owe. 15 percent length of credit history. 10 percent new cards. 10 percent types of credit.

35 percent based on your payment history. 30 percent based on the amount you owe. 15 percent length of credit history. 10 percent new cards. 10 percent types of credit.

FICO TIPS:

- Apply for and open credit accounts if you really need them.

- Don’t open accounts just to have a new card.

- Closing a credit card won’t make the debt go away.

In fact, if you close a credit card it’s likely to factor as a negative in your score. If you clear your bill and don’t ever use it, that may be a problem too. So it’s probably a good idea to pay one bill with it, and keep it in a drawer the rest of the time. ![]()

3 Tips to Manage Credit Card Debt

Also when you use your credit card, make sure that you don’t exceed 50 percent of the limit. If you go beyond 50 percent, bankers advise that you split the debt between two credit cards. That it is likely to improve your credit score.

HOW TO HANDLE OUTSTANDING DEBT

If you want to pay your bills but can’t make the monthly payments, NEGOTIATE.

A company will write off your debt after 180 days, but it is still held against you and you will still have to pay. The company would rather have your money than write off the debt. It’s better for you and them, if you negotiate.

Here’s what to do:

Call the customer service number on the back of the bill. Be very polite. Say that you would like to set up a payment plan. See if you can negotiate a sum that you can actually afford. If the person on the other end of the phone won’t help you, ask to talk to supervisor.

Don’t lose your temper.

Explain what you want. You are likely to get it.

If you don’t, do a Google search. Find the name of the company president and the address and write a letter explaining what you want to do.

Watch the Video:

i just want a credit report

We continue to get the same answers from the credit reporting companies. They say they take extra care to make sure the reports don’t fall into the hands of thieves and scammers.